Skip to main content

Skip to main content

You’ve probably been here before.

Your phone is broken, and you need to buy a new one. But buying a new phone costs $1000!

You can’t just walk around without a cell phone, so what do you do?

You probably pay a percentage of the phone upfront, say 10% of the total cost, which is $100. Then, you take the phone home to use.

Wait, did you just walk out of the store with a brand-new phone after only paying a tenth of the phone’s price?

Probably not.What you did was sign an agreement where, after making a small down payment, you pay on credit for the phone.

This means that you will pay a set price per month to use the product until you have paid the full price, $1000, plus interest.

Leasing a printer from a vendor works the same way.

Sometimes we need to purchase products or items that come with a high price tag, like homes to live in, or cars to drive. If we can’t afford to pay the entire amount upfront without overspending, that is where credit comes in.

Credit gives you the ability to purchase an item now and pay for it over time in small monthly payments. Whenever you apply with a company to lease or buy a product that you can pay for over a period of time, you are subject to a credit check.

Credit acceptance is required to enter into most lease agreements, including leases for copiers and/or printers.

At STPT, we have decades of experience working with lenders and leasing printers to local companies. Over the years, we’ve noticed a few common reasons why companies may not be approved for a lease, and we’ve learned a few tricks to help you get the printers you need.

This article will explain the likelihood of application approval with bad credit when leasing a copier printer.

After reading this article, you will understand what credit is and how it works. You will also learn why credit is denied and what you can do to improve your chances of approval for leasing or purchasing an office printer.

What is Credit & How Does it Work?

Credit is the middleman in the push-and-pull relationship between lenders and borrowers.

A lender, which is usually a bank, credit union, leasing company, or credit card company, checks your creditworthiness and then either approves or denies your borrowing a particular amount of money for purchasing an expensive product on credit.

While borrowing the money or using the product on lease, the borrower must also agree to pay the money back in installments to the lender, often with interest. This is how lenders make money.

Most leasing companies will not allow you to lease a product under the value of $1,000. If you want to lease a small device that costs less than $1,000.00 you need to be prepared to use your banking relationship or a credit card.

For a product that is over $1,000.00, leasing companies will perform a credit check. A lender will determine your creditworthiness before entering into an official agreement with you.

Credit checks assess creditworthiness, and they do this in a few different ways.

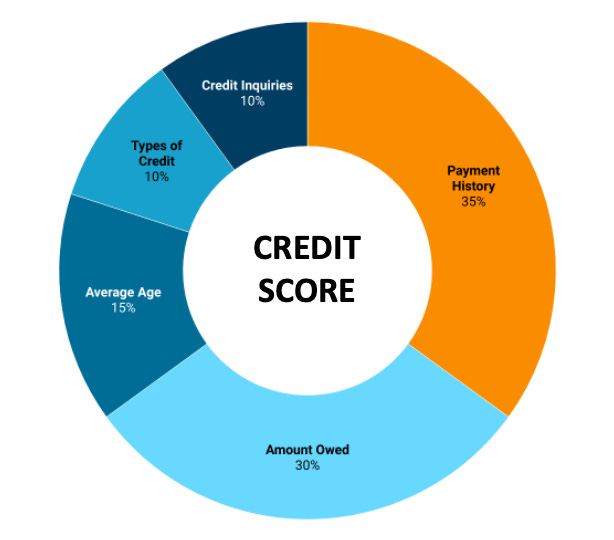

According to the Consumer Financial Protection Bureau, credit checks involve lenders looking at reports based on borrowers’ previous credit usage, spending habits, and income level. These reports use a mathematical formula to determine your credit score.

(See graphic below from Graham Stephan’s newsletter for a more detailed explanation.)

A credit score is a number that predicts your credit behavior based on the information found in your credit report. The score sits on a scale from 300 to 850. These credit score ranges help borrowers and lenders figure whether a score is good or bad for lending.

For example, a good credit score is generally considered to be in the 690 to 750 range, and an excellent credit score would be 750 or above. However, that range is flexible and depends upon the lending institution’s discretion.

There are several things that make you likely to have a good credit history and score for leasing, including good payment history that shows timely payments, the amount of money you owe—also called your debt—and how long your lines of credit have been in use and good standing.

Leasing a Printer with Credit

Obtaining credit for the purchase of a printer is just like getting approved for credit to purchase a car: first, you could be asked to make an upfront payment, and then you can use the car for several years while also making monthly lease payments.

So, if you intend to lease, credit is very important and will be required by any company you choose to do business with.

Although leasing is an option that is very attractive to buyers, it is important that you are prepared before entering into a printer copier lease agreement.

There are three types of copier lease agreements to consider: fair market value, fixed purchase option, and installment purchase. For more information on copier lease agreements, check out our Comprehensive Guide to Copier Lease Agreements.

If you want to lease a copier printer, then there are other things to consider as well, such as whether you should lease or purchase a machine and which printer fits your budget.

But for now, let’s focus on credit approval:

Reasons Why Your Credit Won’t Be Approved

To get approved for a lease contract, you need to have good credit.

If your credit or your company’s credit is not well established, then it is possible your credit will not be approved for printer copier leasing. There are many reasons why this may happen.

Lenders’ comfort of risk is constantly changing. However, common issues that affect your likelihood to be approved for a line of credit include:

Your Business’s Credit History is Too Recent

Length of credit history also affects your credit score and your likelihood of being approved for a lease contract.

Experian explains that your length of credit history is determined by the average age of all your open credit accounts, how old your oldest account is, and how long it has been since your newest line of credit was opened.

This means that newer businesses, or companies that have only been open to use credit for a short period of time, may not have enough credit history to substantiate their ability to make payments on time.

According to a FICO study, the average length of time needed to establish an excellent credit score (in the 800+ range) is about 10 years, so if your business is less than 10 years old, then your credit may not be established enough for approval.

Lenders consider this information pertinent to your credit approval because it is a risk to lend to a business that does not already have an established history of timely payments.

Your Credit Report Shows Many Missed or Late Payments

Credit is subject to past spending and payment history.

This means that your business needs to have a history of on-time payments to impress lenders.

Missed or late payments have a huge impact on your credit approval, and many vendors will not be able to lease to a business whose credit report shows many delinquencies.

Income to Debt Ratio

If your company’s credit history shows many late payments or your business is too new to have an established credit history, then you may need to use your personal credit to support your company’s application for a lease with a personal letter of guarantee (more on this later.)

If your business requires a personal letter of guarantee for the loan application, then your income to debt ratio will also be considered by a lender when determining your likelihood for credit approval.

Put simply, lenders check how much money you pay monthly on debts (mortgages, leases, credit card payments, etc.) and then they divide that number by the amount of your monthly income. This number is how lenders figure your ability to make payments.

If your ratio of debt to income is too high, meaning more than one-third of your income goes towards debt repayments, then your credit may not be approved for a lease because the lender has crunched the numbers and believes you cannot afford to pay the amount required.

The Consumer Financial Protection Bureau offers a simple breakdown of this here if you would like more information.

What to Do About It

If your business has more than two years of operating history, pays bills on time, and has a greater income to debt ratio, then the business is likely to be approved for a lease agreement.

However, if your business does not fit those criteria, there are still a few things you can do to boost your chances of approval for a copier printer lease.

If your business is new and does not have any credit history and your personal credit is healthy, then a personal letter of guarantee is a good option for you.

A personal letter of guarantee is a good way to use your personal credit to help build your business credit as you get the business up and going.

Another option is to make a larger down payment on the printer copier. This would lower the financed amount and show good faith to your lender because you are able to pay a large sum of money upfront for the purchase.

Local relations with banking institutions are always a good practice. If a local banking institution knows you personally, they may be more likely to provide your business with credit. However, it is also likely they have the same basic requirements for loaning out their money as most leasing institutions, which could make it difficult for them to ignore bad or unapproved credit.

Sometimes you can ask your print vendor for a short-term three-month payout, which lowers the risk for the vendor and allows them to accept the deal.

Remember: your vendor wants to make the sale as much as you do. They will likely try to make the deal with multiple leasing companies since some are more willing to accept different credit risks than others. As a note, changing leasing companies could affect your proposed monthly payment.

The equipment vendor is just as disappointed as you when credit denials occur.

What’s the Best Way to Buy or Lease a Printer?

Lenders don’t like to take risks, so why should you?

STPT is a print vendor that wants you to be informed so you can make educated decisions about leasing or purchasing office equipment for your business.

As a vendor who has been in the business for over 30 years, we have experience working with lenders and borrowers to make the deals small businesses need to get access to quality Xerox branded printer copiers.

It is our goal to help you through the buying process, so please reach out to us if you have any questions or concerns about credit approval for printer leasing.